8 Real Estate Trends Influencing Your Business Now

Relocation buyers are moving greater distances. Cash buyers are tough competitors. The relief in home prices likely is over. Know the factors impacting your clients’ home search the most.

The real estate market is poised for better days ahead as the short-lived “housing recession” comes to an end.

Lawrence Yun, chief economist at the National Association of REALTORS®, said Wednesday during NAR’s quarterly Real Estate Forecast Summit that bidding wars have returned as homebuyer demand soars, even as inventory remains sparse. The number of homes on the market remains historically low while Americans’ aspirations to become homeowners remains high. “Home sales are likely bottoming out this year before an upturn next year,” Yun predicted. “But it’s contingent on mortgage rates falling.”

Yun and Jessica Lautz, NAR’s deputy chief economist and vice president of research, provided a breakdown of the top trends they’re noticing in the housing market.

1. Doom-and-gloom headlines are overblown. While the housing market is correcting after pandemic-fueled highs, with existing-home sales plunging 19% year over year, that doesn’t mean a long-term rut is forming. “I keep hearing people say they’re waiting for prices to drop,” Lautz said. “But if you look at the data, that’s just not happening right now. You may see some home price differences in just one state and then see some big headlines—but the skies are not falling.”

In fact, there are more than three offers for every listing on average, according to NAR data, and about a third of homes on the market nationwide are selling above list price. Although distressed sales—foreclosures and short sales—have seen a modest uptick, they remain at historical lows and likely won’t grow much more, Lautz said. “Homeowners have equity, so even if they do face a life event, they will likely still have enough equity to cover their mortgage.”

2. Americans are moving longer distances. From 1981 to 2021, the average home buyer moved just 10 to 15 miles away from their previous residence. But over the last year, the average buyer moved a median of 50 miles; a quarter moved more than 470 miles, NAR’s data shows. Buyers are moving for a variety of reasons, Lautz noted, including retirement, proximity to family, housing affordability and the ability to work remotely.

Real estate websites are increasingly important to relocation buyers: “People who move longer distances still use a real estate agent,” Lautz said. “But they’re increasingly finding their agents online, not by going to family and friends for a referral.” Also, these long-haul movers are more likely to use technology, such as virtual tours, in their home search, she added.

3. Cash buyers remain formidable competitors. Twenty-six percent of the marketplace consists of cash buyers, which is substantially higher than before the pandemic, Lautz said. These buyers are mostly investors and property owners who have built equity and can pay for a second home in cash. They’re proving to be steep competition for first-time home buyers, who tend to have smaller down payments, Lautz added.

4. Generational dynamics are at play. The median age of a first-time home buyer is 36, reflecting a cultural shift toward entering homeownership later in life than did past generations. A lack of affordable inventory is pressing on young adults’ ability to buy, Lautz noted. FHA and VA loans, which help many underserved buyers, have lower down payment options and may be key to bringing more young adults into homeownership, she added.

Baby boomers have usurped millennials as the strongest homebuying force in America, with the elder group comprising 39% of the market compared to 28% for young adults, according to NAR data. “Millennials have been priced out and are often losing out to cash buyers,” Lautz said. Baby boomers, many of whom have accumulated housing wealth over decades, appear motivated to move so they can live closer to family, buy their “forever home,” have a smart home and even live with roommates.

5. New construction is a bright spot in the market. While existing inventory is at historical lows, the new-home market is offering more options to buyers, Yun said. New-home sales typically make up 10% of the market—but they are currently running at 20%, he added. NAR predicts new-home sales to rise 12.3% in 2023 and 13.9% in 2024.

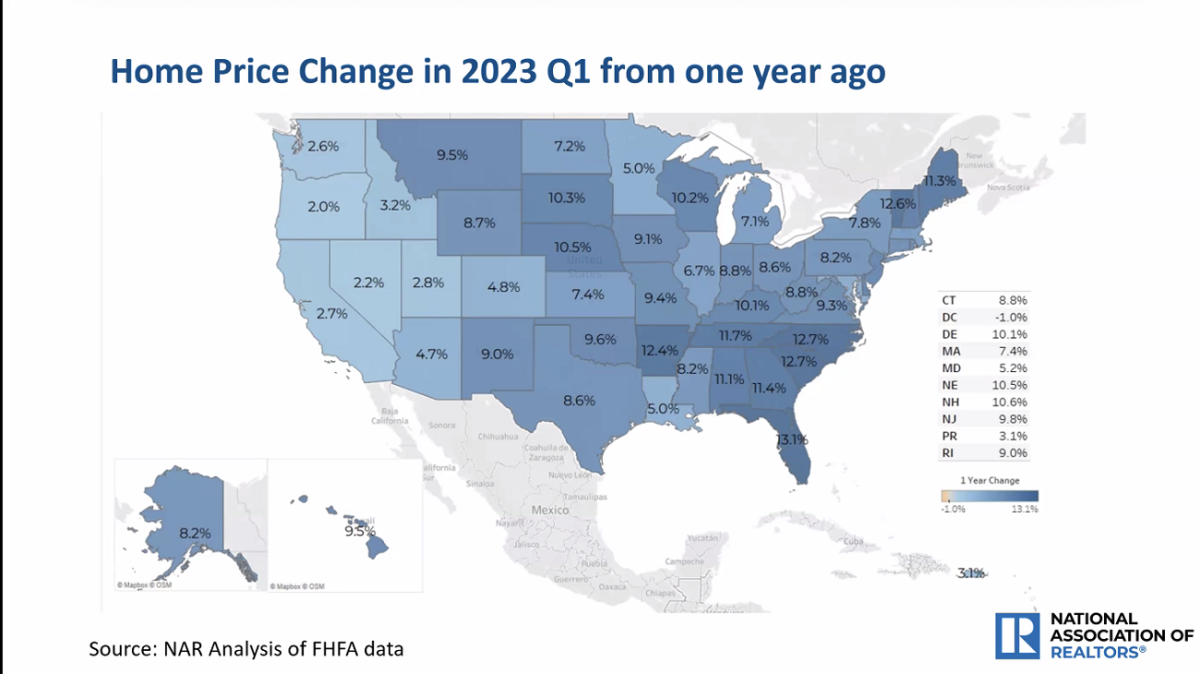

6. Home prices likely won’t fall any further. Home prices are down 1% compared to a year ago, Yun said. There are geographic variations: San Francisco, for example, has seen home prices drop 15% year over year. “But overall, I think the decline is over,” he said.

Other price measurements, like the FHFA’s House Price Index, are beginning to show acceleration in month-to-month home prices. Also, the median sales price for an existing home in June surged to $410,200—the second-highest level in more than two decades, according to NAR data.

“While there may be little changes to prices from one quarter to the next, the long-term perspective is that housing has brought great wealth accumulation for homeowners,” even those who have purchased in the last two years, Yun said. Further, home prices remain higher compared to a year ago in practically every U.S. market. NAR has forecasted home prices to rise by 2.6% in 2024.

7. Mortgage rates are likely to decline somewhat. Yun said he’s hopeful that mortgage rates will soon cool from their near-7% averages, which has increasingly pressed on home buyers’ budgets. However, Fitch Ratings on Tuesday downgraded the U.S. debt rating, which could bump up borrowing costs. Yun said the Federal Reserve’s next decision on short-term interest rates at its meeting in late September will influence the direction of long-term borrowing costs. If the Fed stops raising its short-term rates, and if inflation continues to edge down, the 30-year fixed-rate mortgage could fall near 6% by the end of the year, Yun said.

8. Inventory is housing’s most pressing problem. Homebuying demand is high while housing inventory is at historical lows. Seventy-six percent of homes sold in June were on the market for less than a month, according to NAR data. The association has been calling on lawmakers to do more to help supply meet demand.

NAR supports tax incentive proposals for those who sell a residential property being used as a rental to an owner-occupied buyer. “We’re hoping we can get lawmakers to listen,” Yun said. “We need to get immediate inventory onto the marketplace.”

The national homeownership rate may have peaked already, considering the barriers keeping first-time buyers from entering the market, Yun said. “If we continue to restrict supply, prices will skyrocket and homeownership will slow.”

Source: REALTOR® Magazine