Housing Market Reports

Stay informed with MetroTex’s monthly and annual market reports, featuring data from Texas A&M Real Estate Research Center.

Texas A&M housing statistics are based on listing data from over 50 multiple listing service (MLS) systems in Texas. These statistics are calculated based on listings of properties physically located within the specified geographic areas.

Texas Housing Insight

March 2026

The 2026 market opened with rising seller activity, elevated inventory levels, and persistent pricing pressure as affordability challenges continue to shape buyer demand.

Housing Reports

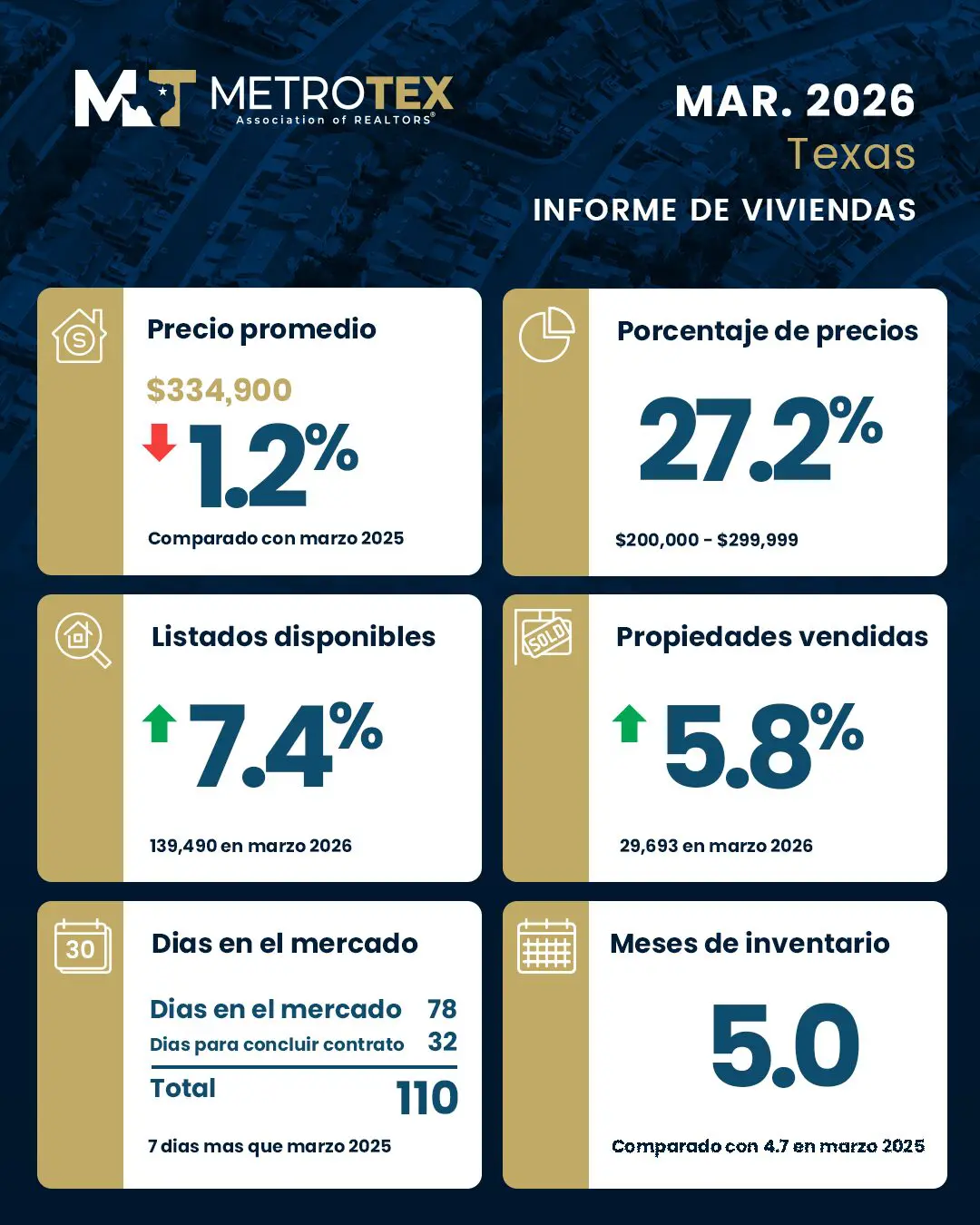

Texas

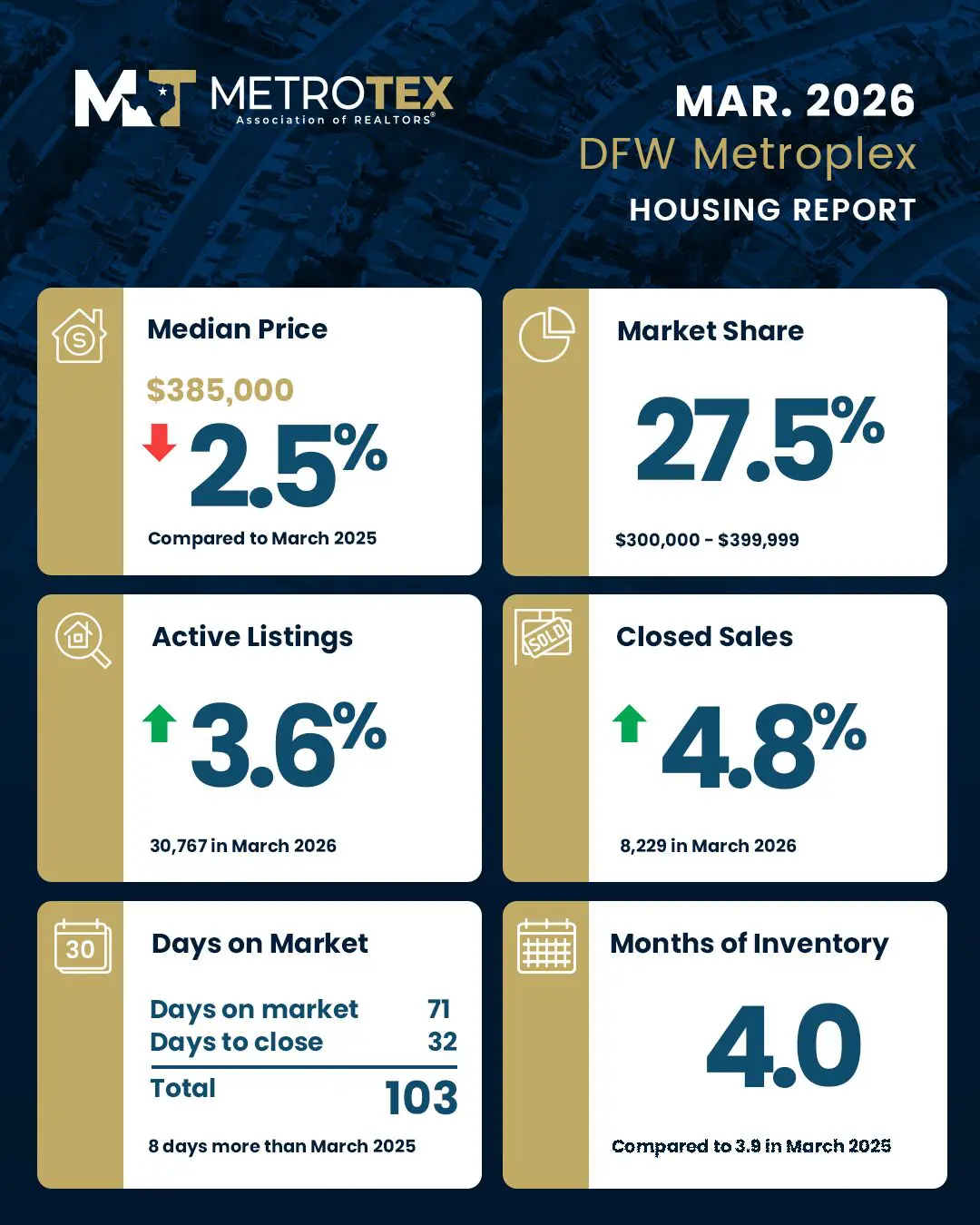

DFW Metroplex

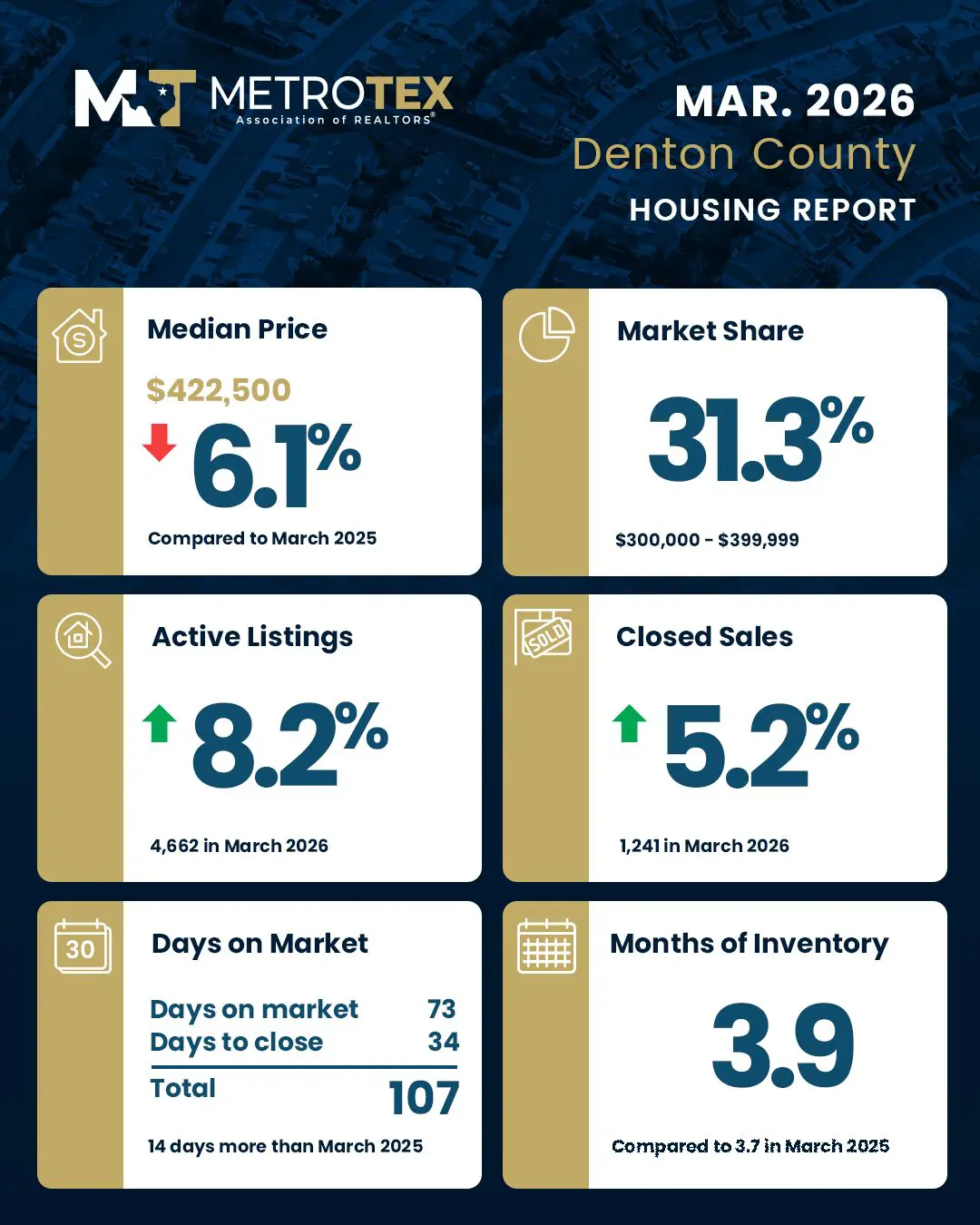

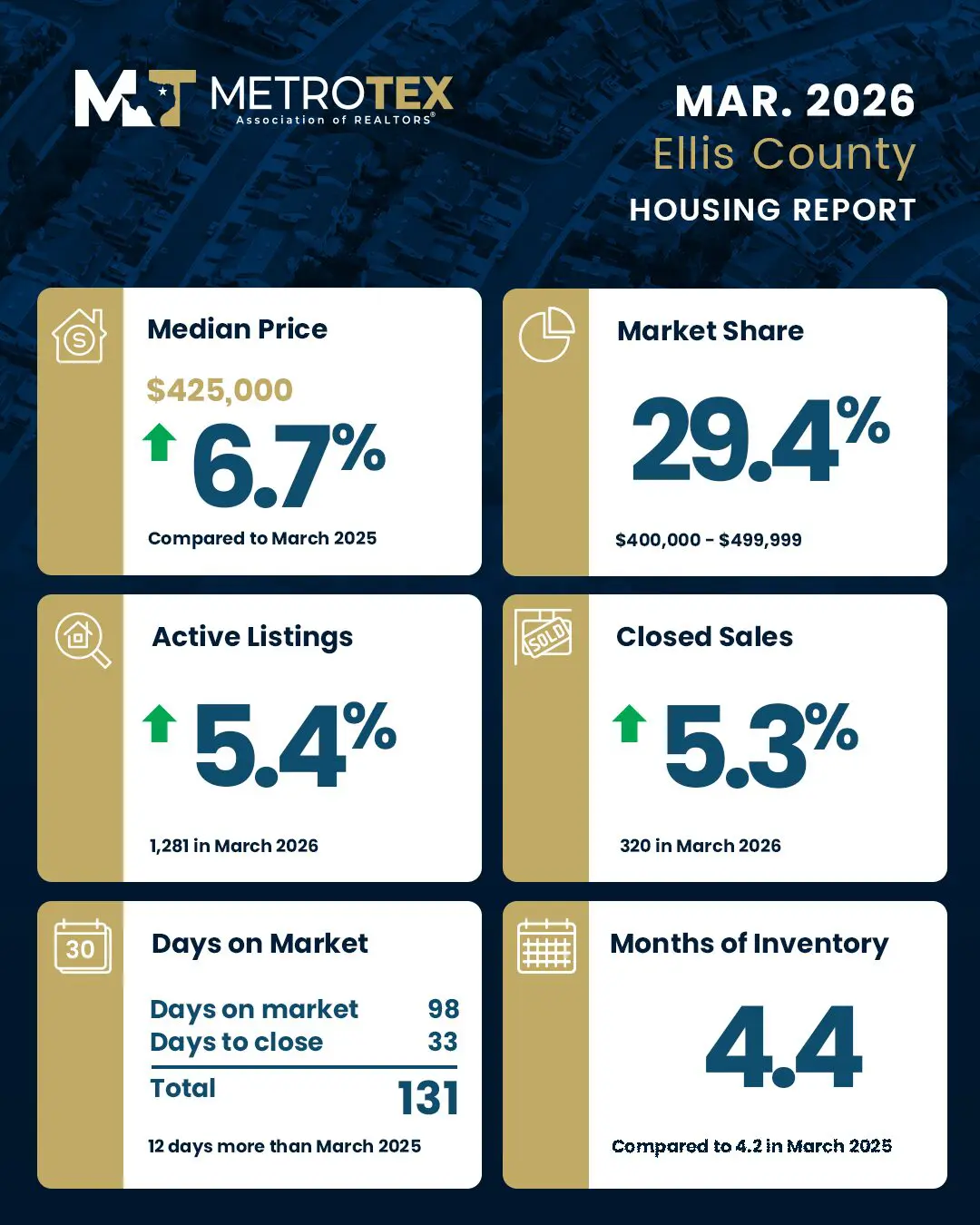

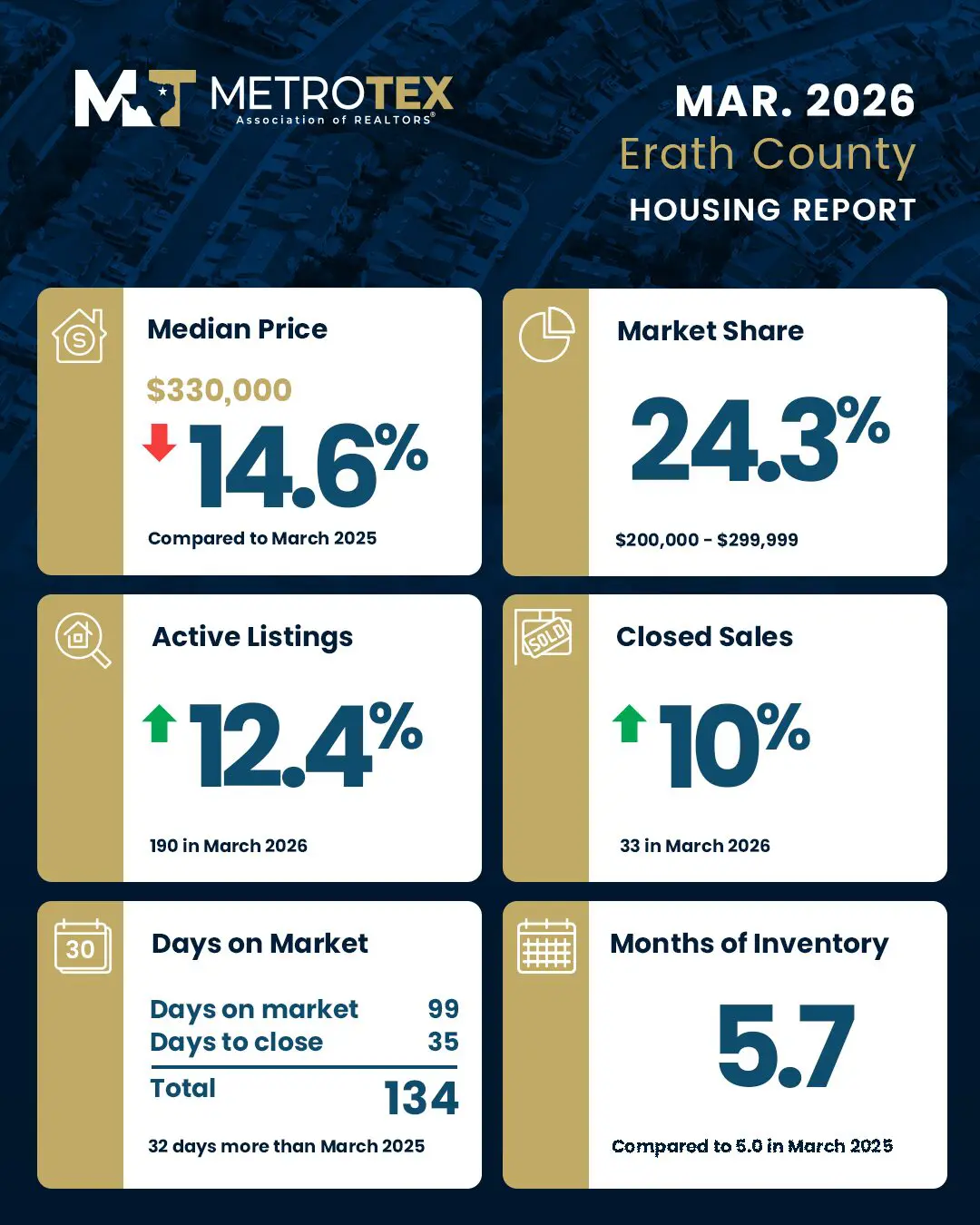

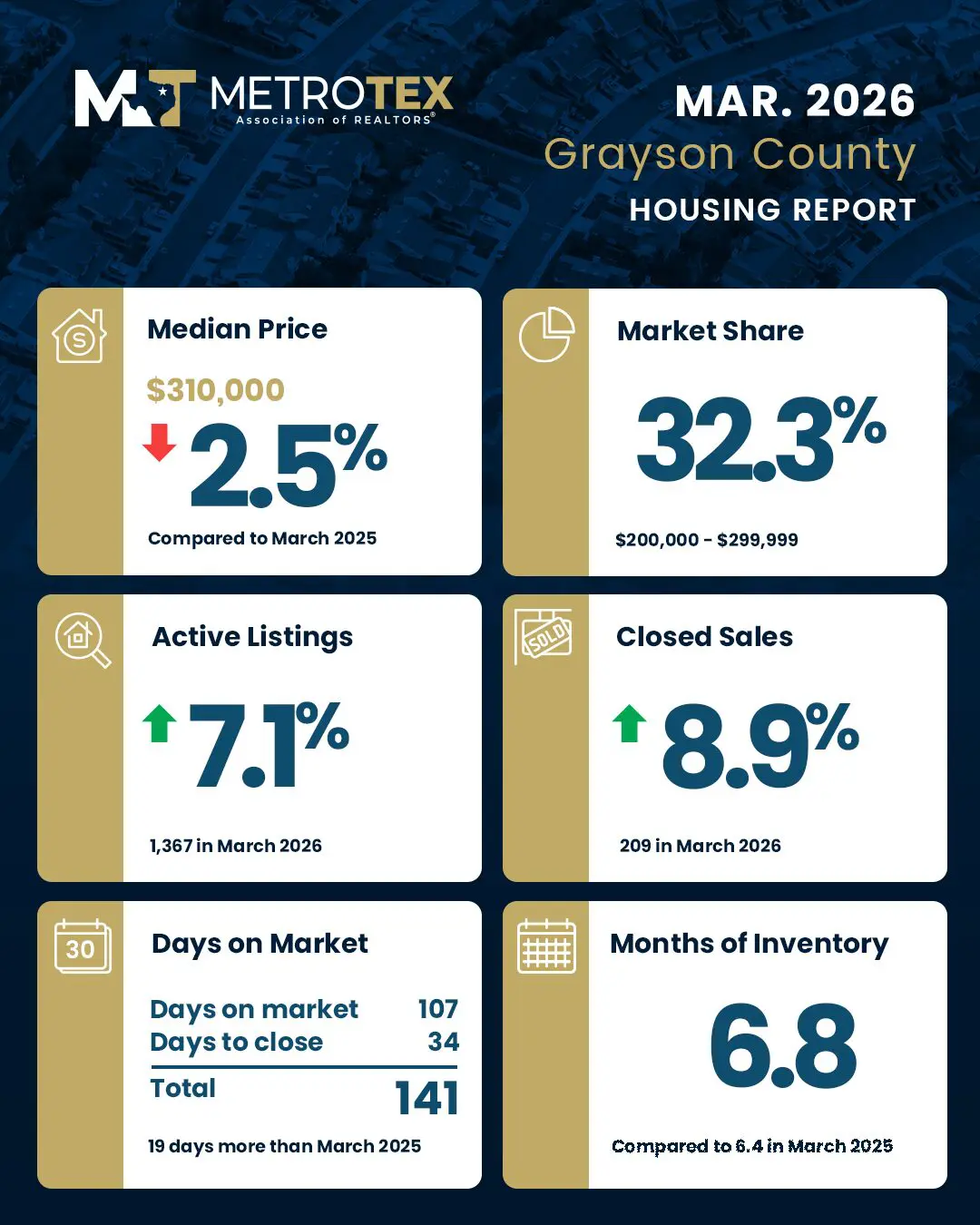

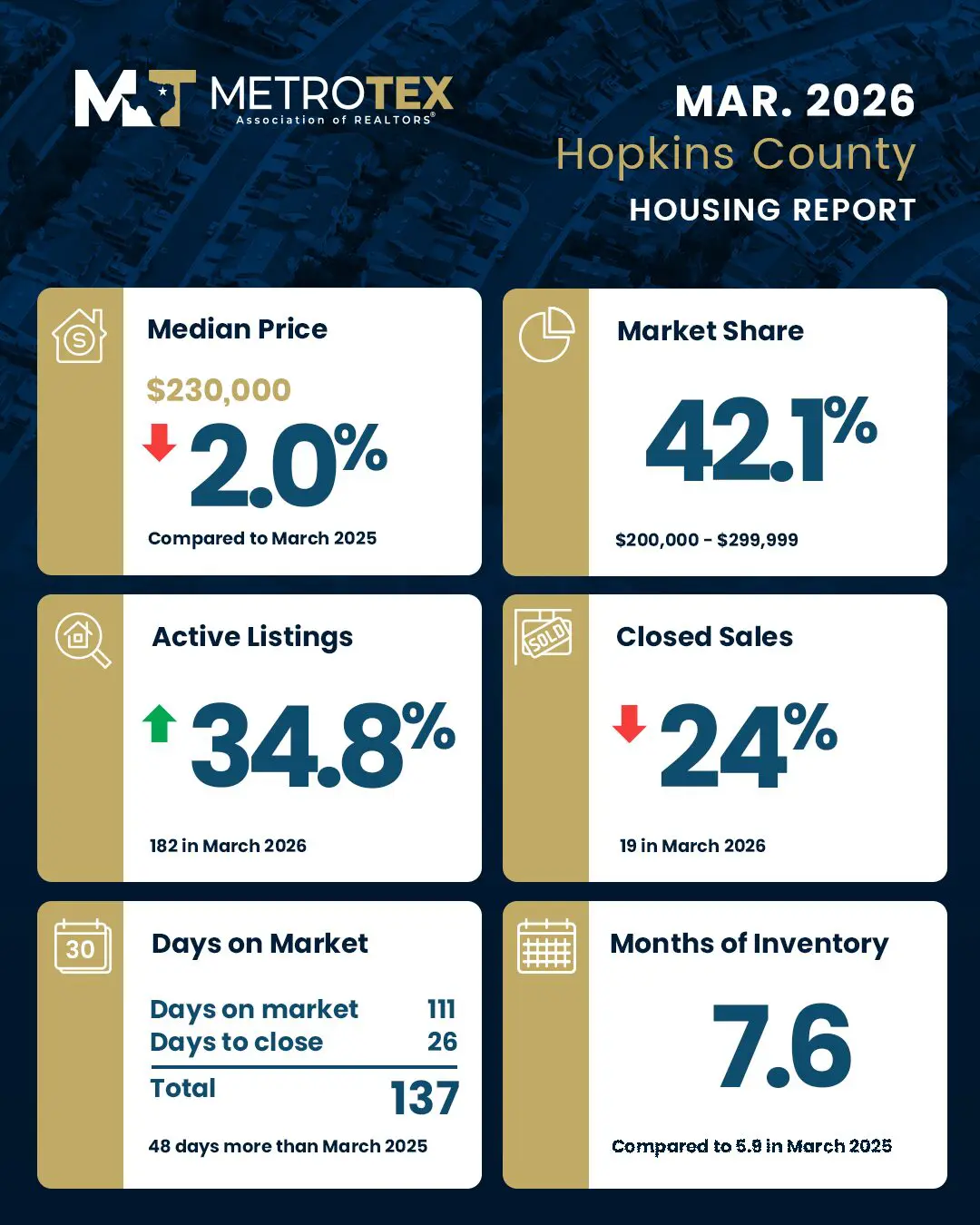

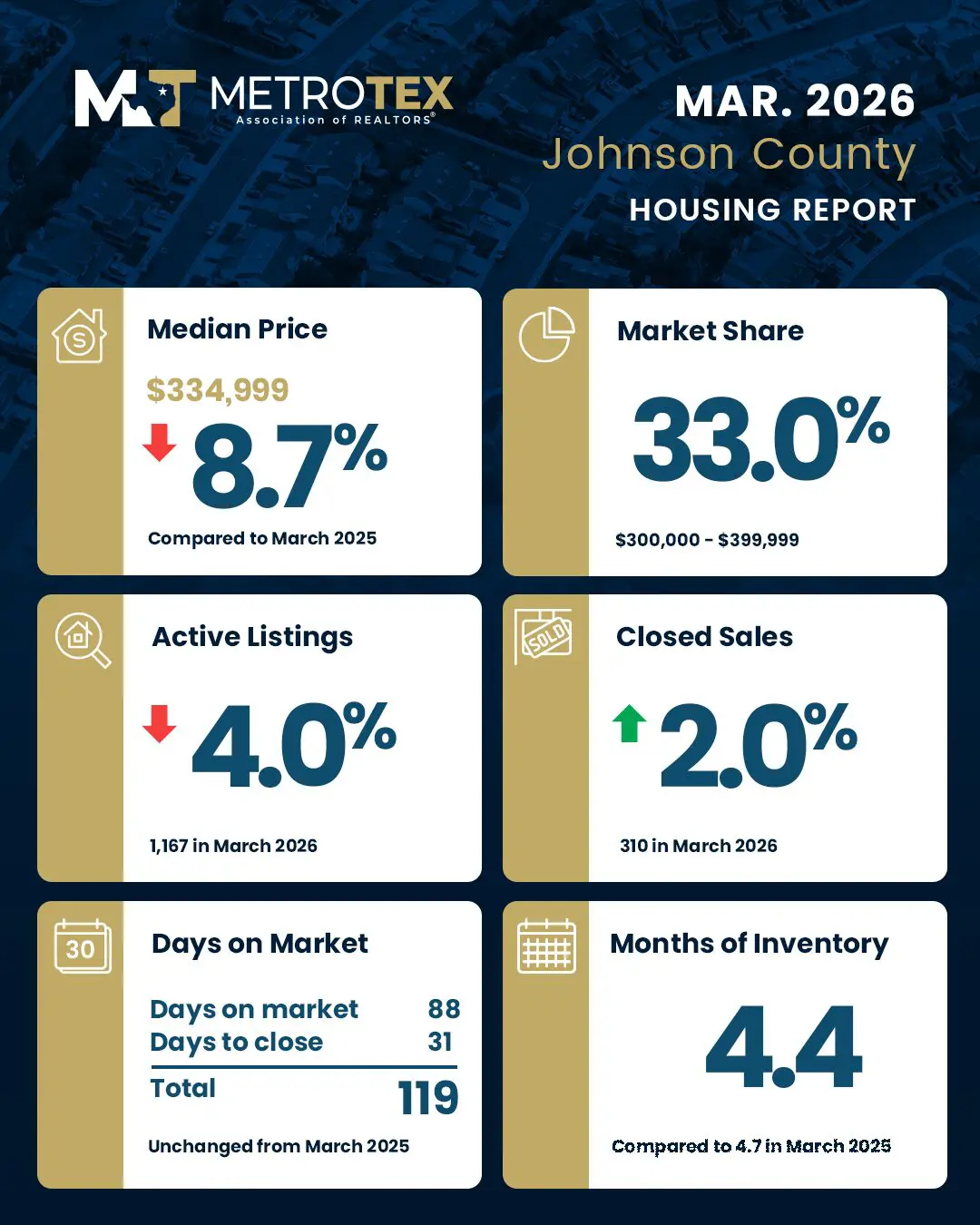

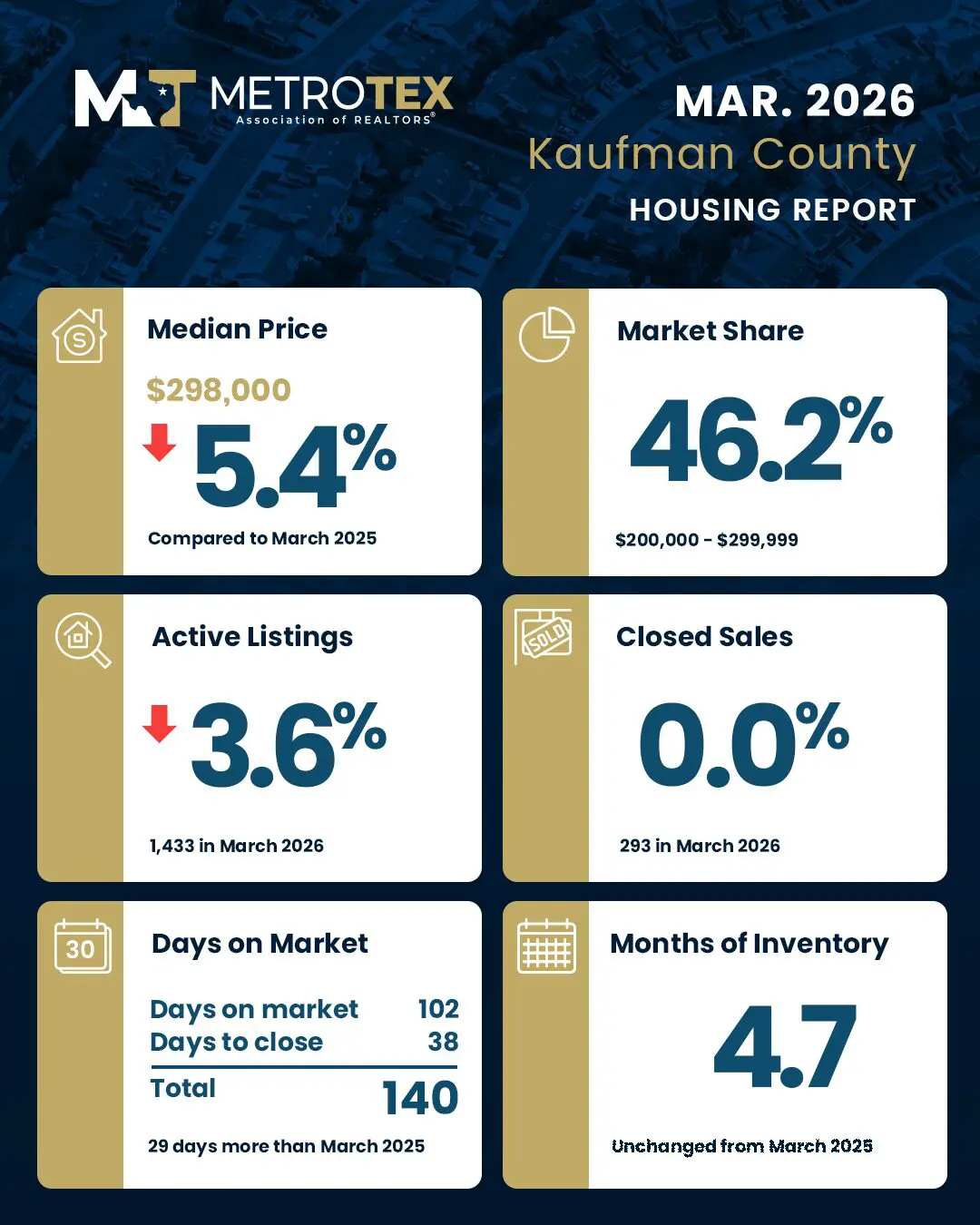

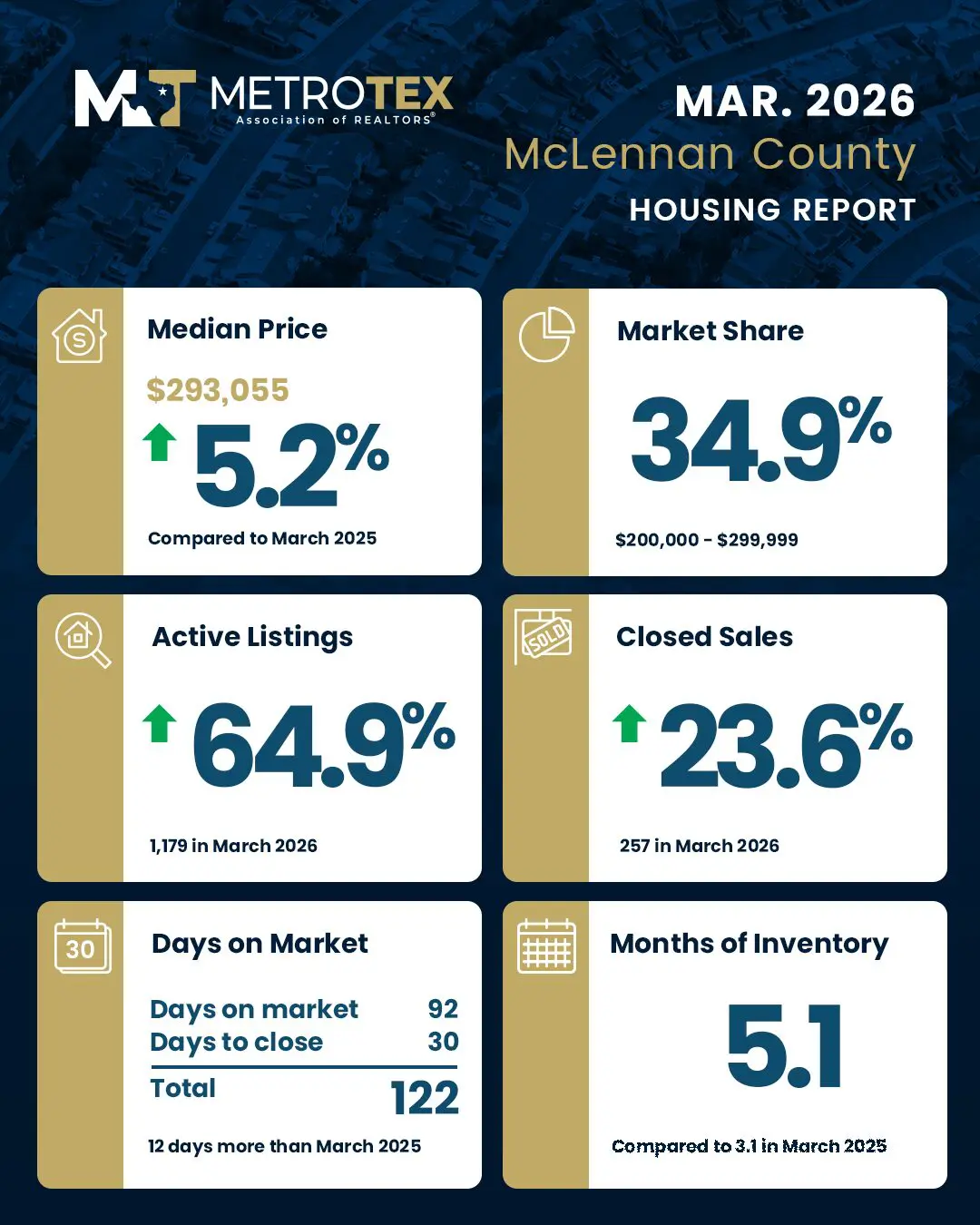

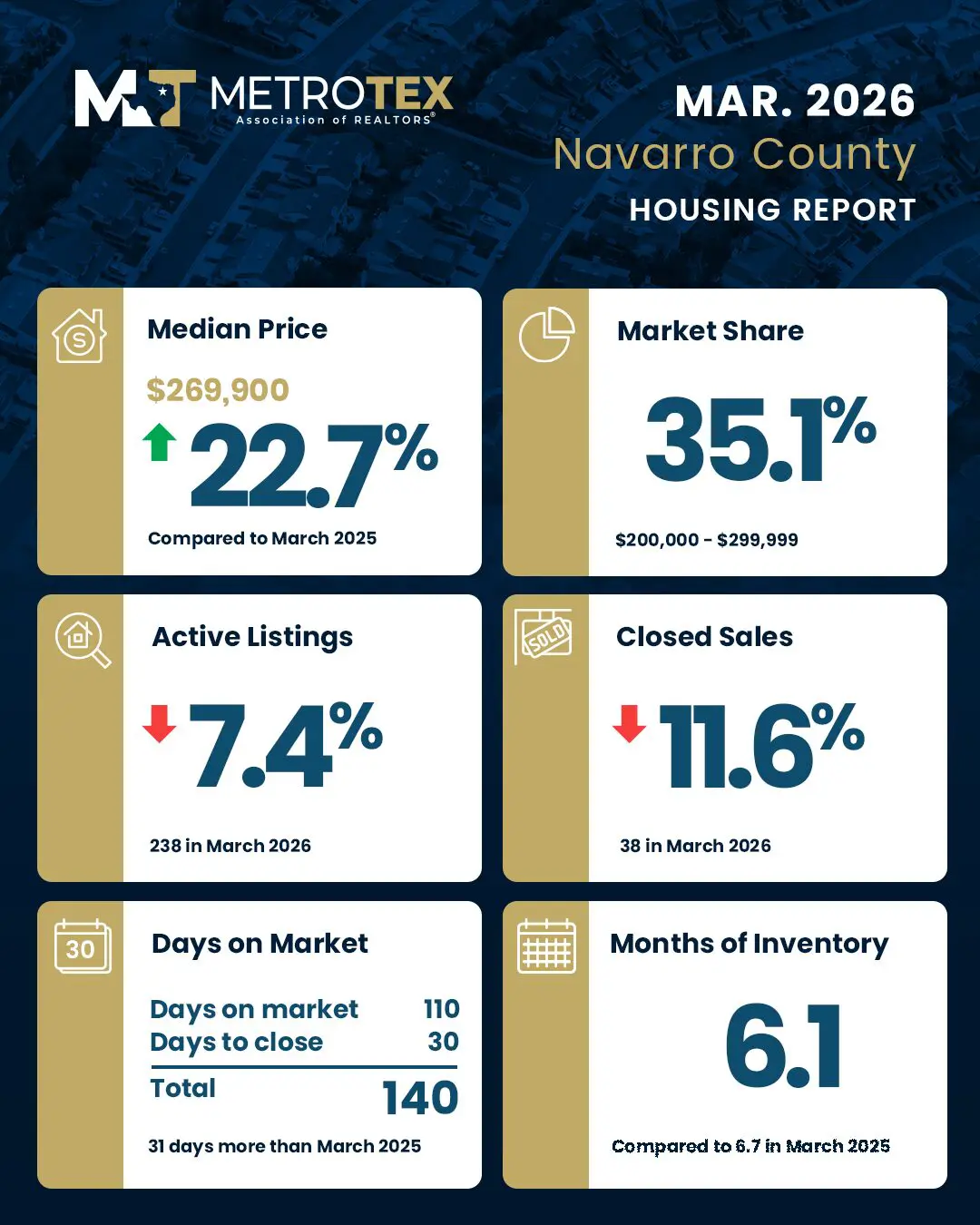

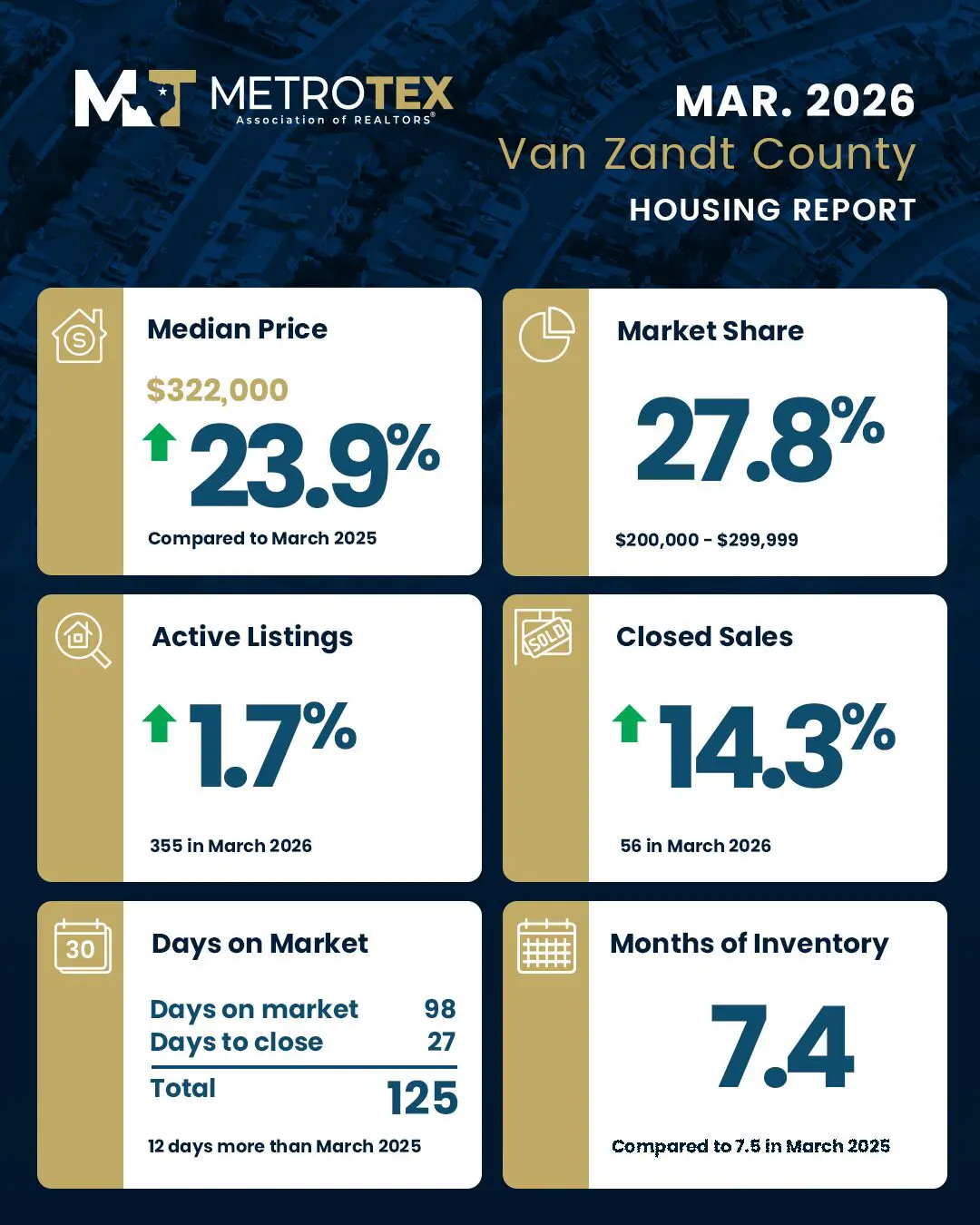

2026 Reports

MetroTex provides current and relevant monthly and annual data reports with the support of the Texas Real Estate Research Center at Texas A&M University.![]() Note: NTREIS no longer provides boundary data for MLS defined areas; therefore, that section of the report has been removed.

Note: NTREIS no longer provides boundary data for MLS defined areas; therefore, that section of the report has been removed.

Previous Reports

Texas A&M Data Series Descriptions

Housing Activity

Data Series Description

Housing statistics are based on listing data from over 50 MLS (Multiple Listing Service) systems in Texas. Statistics for each geography were calculated based on listings of properties physically located within the mapped area presented with the statistics.

Geographic Definitions

Metropolitan Statistical Area (MSA): Based on the multi-county area specified by The Office of Management & Budget in 2013.

Local Market Area (LMA): An area defined by the local Association/Board of REALTORS representing a logical market of homes that can be grouped together for meaningful statistical reporting.

Getting More Detail

For more detailed statistics about local areas, existing vs. new homes and breakout by property type, contact your local REALTOR® association. Click here for a list of contacts.

Data Release Dates

Statistics for geographies outside of the Houston metro area will be released on/near the 20th calendar day after month end. Statistics for the Houston metro area will be released on/near the 40th calendar day after month end.

2025 Reports

January 2025 Texas A&M Housing Market Report

February 2025 Texas A&M Housing Market Report

March 2025 Texas A&M Housing Market Report

April 2025 Texas A&M Housing Market Report

May 2025 Texas A&M Housing Market Report

June 2025 Texas A&M Housing Market Report

July 2025 Texas A&M Housing Market Report

August 2025 Texas A&M Housing Market Report

September 2025 Texas A&M Housing Market Report

October 2025 Texas A&M Housing Market Report

2024 Reports

January 2024 Texas A&M Housing Market Report

February 2024 Texas A&M Housing Market Report

March 2024 Texas A&M Housing Market Report

April 2024 Texas A&M Housing Market Report

May 2024 Texas A&M Housing Market Report

June 2024 Texas A&M Housing Market Report

July 2024 Texas A&M Housing Market Report

August 2024 Texas A&M Housing Market Report

September 2024 Texas A&M Housing Market Report

October 2024 Texas A&M Housing Market Report

2023 Reports

January 2023 Texas A&M Housing Market Report

February 2023 Texas A&M Housing Market Report

March 2023 Texas A&M Housing Market Report

April 2023 Texas A&M Housing Market Report

May 2023 Texas A&M Housing Market Report

June 2023 Texas A&M Housing Market Report

July 2023 Texas A&M Housing Market Report

August 2023 Texas A&M Housing Market Report

September 2023 Texas A&M Housing Market Report

October 2023 Texas A&M Housing Market Report

2022 Reports

January 2022 Texas A&M Housing Market Report

February 2022 Texas A&M Housing Market Report

March 2022 Texas A&M Housing Market Report

April 2022 Texas A&M Housing Market Report

May 2022 Texas A&M Housing Market Report

June 2022 Texas A&M Housing Market Report

July 2022 Texas A&M Housing Market Report

August 2022 Texas A&M Housing Market Report

September 2022 Texas A&M Housing Market Report

October 2022 Texas A&M Housing Market Report